Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

This research is based upon the most recent available data in 2022–2023. Unless otherwise stated, dollar figures from earlier years are adjusted for inflation to make them consistent in purchasing power with modern dollars.

In keeping with Just Facts’ Standards of Credibility, all charts in this research show the full range of available data, and all facts are cited based upon availability and relevance, not to slant results by singling out specific years that are different from others. Likewise, data associated with the effects of education in different geographical areas represent random, diverse places in which such data is available.

Many of the facts in this research reveal associations between education and other variables. These relationships may be caused in part (or whole) by factors that are related to education but not necessarily caused by education. For example, individuals with high intelligence and discipline tend to excel in education and obtain more of it, but they also tend to earn more money regardless of their education. Hence, the higher earnings of people with more education can be caused by factors beyond their education.[1] [2] [3] [4] [5]

Likewise, student achievement is often affected by family and cultural influences. Thus, the test scores of students at certain schools may be caused by factors other than the schools.[6] [7]

In attempting to isolate the effect of a single factor on a certain outcome, researchers often use statistical techniques to “control” for the effects of other variables. However, these techniques cannot objectively rule out the possibility that other factors are at play. This is called “omitted variable bias.”[8] [9] [10] [11] [12] [13] Moreover, the most common method used to control for multiple variables is prone to other pitfalls that can lead to false conclusions about causes and effects.[14] [15] [16] [17]

In the social sciences, the surest way to determine the effect of one factor upon another is by examining random, experimental data. An example of this is the outcomes of students who won and did not win a random lottery for admission to a certain educational program. Studies of such data can control for the impact of all confounding variables and allow for sound conclusions about cause and effect. However, these analyses sometimes have defects and should be interpreted with caution.[18] [19] [20] [21] [22] [23] [24] [25]

* In 2022, federal, state, and local governments in the U.S. spent $1.2 trillion on education.[26] This amounts to $8,993 for every household in the U.S.,[27] 4.6% of the U.S. gross domestic product,[28] and 14% of government current expenditures.[29] [30] These figures don’t include:

* Government education spending in 2022 was comprised of:

* Relative to other types of government spending in 2022, education spending was:

* During 2022, private consumers and nonprofit organizations in the U.S. spent about $399 billion on formal education. This amounts to 1.6% of the U.S. gross domestic product and $3,039 for every household in the U.S.[42] [43] [44] [45] [46]

* Relative to other spending by private consumers and nonprofit organizations in 2022, education spending was:

* In 2021, U.S. residents aged 25 to 64 reported average cash earnings of $54,252.[48] Cash earnings do not include non-cash compensation, such as employee fringe benefits.[49]

* In 2021, 79% of U.S. residents aged 25 to 64 reported at least some cash earnings, and 21% did not report any cash earnings.[50]

* Among U.S. residents aged 25 to 64 who reported cash earnings in 2021, the average was $68,900. Among the same group, the median was $51,000.[51]

* Click here for more data on education and earnings.

* Per the U.S. Department of Education:

* Per a book about productivity published by the International Labour Office:

* In 2017, the U.S. Department of Education assessed the reading, math, and computer skills of U.S. residents aged 16–65 years. The assessment was nationally representative of people who live in households and excluded the homeless and people in group quarters like prisons and psychiatric institutions.[55] [56] [57]

* The test takers were allowed to use calculators and take as much time as they needed.[58]

* The actual questions on the test are not available to the public, but here are some sample questions:[59]

* In 2003, the U.S. Department of Education assessed the English and math skills of U.S. residents aged 16 and older. The full assessment was nationally representative except for 5% of the population who were completely illiterate in English and Spanish or unable to answer very simple questions.[69]

* Below are some examples of the questions posed in the full assessment, along with the portions of people who answered them correctly:

* Horace Mann, the “father” of the U.S. public education system,[75] [76] claimed in 1841:

* Various federal agencies have reported that two-thirds to three-quarters of all 17- to 24-year-olds in the U.S. are unqualified for military service because of poor physical fitness, weak educational skills, illegal drug usage, medical conditions, or criminal records:

* A 2001 study of high school dropouts published in the American Economic Review found:

* In 2022, federal, state, and local governments in the U.S. spent $834 billion on K–12 education. This amounts to $6,354 for every household in the U.S.[84]

* In the 2019–20 school year, governments in the U.S. spent an average of $17,013 for every student enrolled in K–12 public schools.[85] [86] This figure doesn’t include:

* A scientific, nationally representative survey commissioned in 2021 by the journal Education Next and the Kennedy School of Government at Harvard University found that U.S. adults on average estimate that their local public schools spend $8,719 per student.[101] [102]

* The average class size in public schools is 20.2 students.[103]

* In the 2019–20 school year, the average spending per public school classroom was about $343,663.[104] This excludes the items in the bullet points above.[105]

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 53% of voters believe the average spending per public school classroom is less than $150,000 per year.[106] [107]

* Excluding the items in the bullet points above, the average inflation-adjusted spending per public school student has risen by 27% since 2000, 105% since 1980, 4.0 times since 1960, and 24 times since 1920:[108]

* Since at least the early 1970s:

* Since at least 1994, school districts with higher portions of poor students have spent about the same average amount per student as school districts with smaller portions of poor students.[116]

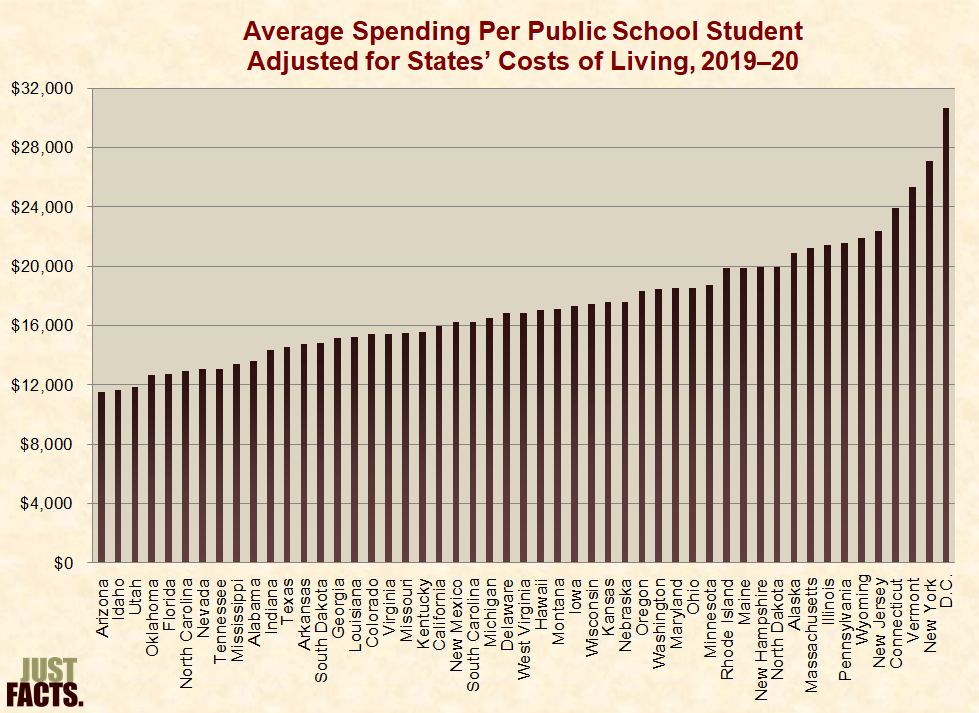

* Adjusted for the cost of living in different states, the average spending per public school student in the 2019–20 school year ranged from $11,481 in Arizona to $30,682 in the District of Columbia. (This excludes state administration, unfunded pension liabilities, and non-pension post-employment benefits.[117])

* In the 2019–20 school year, private consumers, nonprofit organizations, and governments spent an average of about $9,709 for every student enrolled in private K–12 schools.[119] [120] [121] [122] [123] [124]

* The average class size in private schools is 15.3 students.[125]

* In the 2019–20 school year, the average spending per private school classroom was about $148,548.[126]

* In the 2011–12 school year (latest available data), the average full tuition for students in private K–12 schools was $13,310. Full tuition or “sticker price” is “the highest annual tuition charged for a full-time student.” The actual amounts paid by individuals are lower if they receive discounts for reasons such as having low income, siblings in the school, or a parent who is a teacher. For different types of private schools, the average full tuition varied as follows:

|

School Type |

Tuition |

|

Catholic |

$8,539 |

|

Other religious |

$10,769 |

|

Nonsectarian |

$26,657 |

* A nationwide study of 11,739 homeschooled students during the 2007–08 school year found that parents spent a median of $400 to $599 per student on “textbooks, lesson materials, tutoring, enrichment services, testing, counseling, evaluation,” and other incidentals.[129] [130] Regarding these findings:

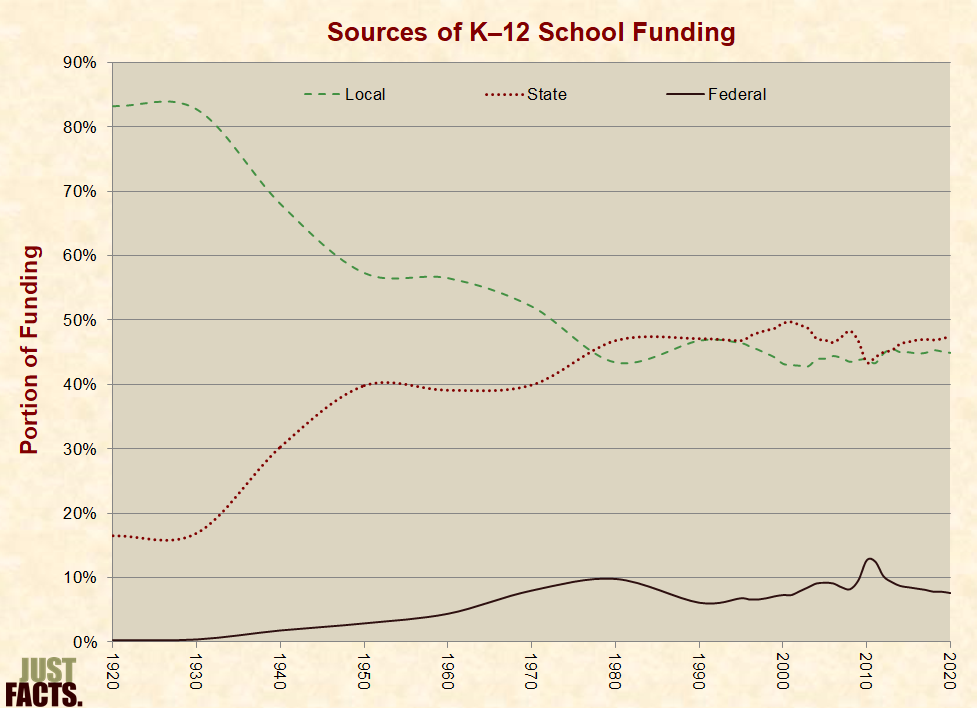

* From 1920 to 2020 the portion of K–12 public school funding provided by:

* In the 2019–20 school year, public school revenues came from the following sources:

|

Source |

Portion of Revenues |

|

Federal Government |

8% |

|

State Governments |

48% |

|

Local |

45% |

|

Property Taxes |

37% |

|

Other Government Revenues |

7% |

|

Private Revenues |

1% |

* In the 2018–19 school year, 52% of public education spending was used for student instruction.[139] (This excludes state administration, unfunded pension liabilities, and non-pension post-employment benefits.[140]) The remainder was spent on:

|

Function |

Portion of Total |

|

Property purchases and building construction |

10% |

|

Operations and maintenance |

8% |

|

Administration |

7% |

|

Student guidance, health, attendance, and speech pathology services |

5% |

|

Instructional staff services, such as curriculum development, training, and computer centers |

4% |

|

Student transportation |

4% |

|

Food services |

3% |

|

Interest on school debt |

3% |

|

Other |

4% |

* In the 2018–19 school year, 69% of public school expenditures were spent on government employee benefits and salaries.[142] (This excludes state administration, unfunded pension liabilities, and non-pension post-employment benefits.[143])

* In 2021, 49% of all compensation for state and local government employees was paid to people who work in education.[144] This includes salaries and benefits.[145] [146] [147] [148] [149] [150]

* In the 2021–22 school year, the average immediate costs to taxpayers of compensating each full-time public school teacher in the U.S. were:

* Immediate costs of compensating teachers don’t include unfunded pension liabilities and non-pension post-employment benefits like health insurance.[152] [153] [154] [155]

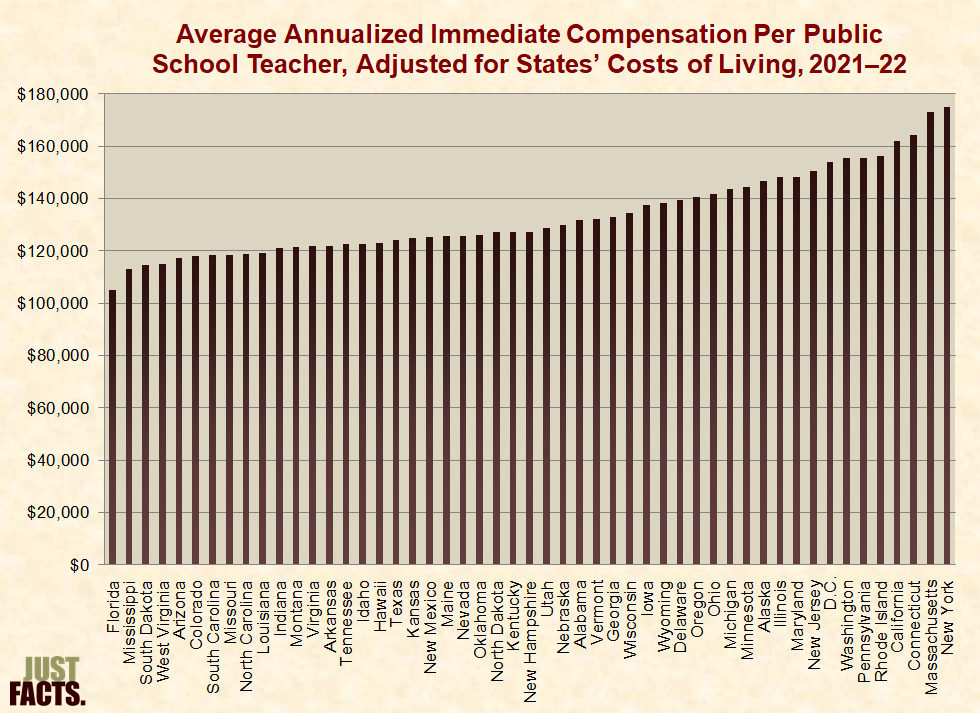

* Adjusted for the costs of living in different states, the average immediate costs of compensating each full-time public school teacher in the 2021–22 school year ranged from $76,463 in Florida to $127,463 in New York.[156]

* Full-time public school teachers work an average of 1,490 hours per year, including time spent for lesson preparation, test construction and grading, providing extra help to students, coaching, and other activities.[157] [158] [159] [160]

* Full-time private industry workers work an average of 2,045 hours per year, or about 37% more than public school teachers. This includes time spent working beyond assigned schedules at the workplace and at home.[161]

* Accounting for the disparity between the work hours of public school teachers and private industry workers, the annualized immediate cost of compensating each full-time public school teacher in the 2021–22 school year was a nationwide average of $137,917.[162] [163]

* Adjusted for the costs of living in different states, the average annualized immediate costs of compensating each full-time public school teacher in the 2021–2022 school year ranged from $104,944 in Florida to $174,940 in New York:

* In the 2020–21 school year (latest data):

* In the 2020–21 school year (latest data), the average base salary for full-time public school teachers was 33% higher than for full-time private school teachers.[167]

* In March 2020, the average immediate cost per contract hour of compensating public school teachers and private school teachers varied as follows:

|

Compensation Component |

Cost Per Contract Hour |

||

|

Public School |

Private School |

Public School Premium |

|

|

Wages and salaries |

$45.29 |

$38.33 |

18% |

|

Benefits |

$23.56 |

$13.22 |

78% |

|

Total compensation |

$68.85 |

$51.55 |

34% |

* The following caveats apply to the data above:

* In the U.S., all 50 states provide children with at least 13 years of taxpayer-financed education from kindergarten through 12th grade.[177]

* The average public school year is 179 days, and the average school day is 6.7 hours not including transportation and extracurricular activities.[178]

* In 2019, approximately 88% of K–12 students were enrolled in public schools, 10% were enrolled in private schools, and 2% were homeschooled.[179] [180]

* Among public school students who began high school in 2016, 87% graduated within four years. This was true for:

* In 2021, U.S. residents aged 25 to 64:

* Click here for more data on education and earnings.

* In 2022, 37% of high school students who graduated that year took the ACT college readiness exam.[184] Among these graduates, 22% met ACT’s college readiness benchmarks in all four subjects (English, reading, math, and science). For each subject, the rates of college readiness were as follows:

* Among high school students who graduated in 2022 and took the ACT college readiness exam, the following racial/ethnic groups met ACT’s college readiness benchmarks in all four subjects:

* From 2010 to 2021, the average GPA of high school students who took the ACT college readiness exam test rose by 5%, while their average ACT test score fell by 3%. Per ACT, “This suggests the presence of grade inflation” because “scores on a standardized measure of achievement” declined while GPAs increased.[187]

* In 2019, the U.S. ranked 5th among 36 developed nations in average spending per full-time K–12 student. The average spending per U.S. pupil was 38% above the average of these nations.[188] [189]

* In math tests administered by the International Mathematics and Science Study to 4th grade students during 2015, U.S. students ranked 14th among 48 nations. The average score of U.S. students was 8% above the average of all tested nations.[190]

* In math tests administered by the Program for International Student Assessment to 15-year-old students during 2018, U.S. students ranked 31st among 37 developed nations. The average score of U.S. students was 2% below the average of all tested nations.[191] [192] [193]

* U.S. students outperformed the following nations on the 4th-grade math exam but underperformed them on the 15-year-old math exam: Australia, Canada, Czech Republic, Finland, France, Germany, Hungary, Italy, Lithuania, Netherlands, New Zealand, Poland, Slovenia, Sweden, and Slovak Republic. U.S. students did not move ahead of any other nation between the 4th grade and 15 years old.[194] [195]

* In reading literacy tests administered by the Progress in International Reading Literacy Study to 4th grade students during 2016, U.S. students ranked 15th among 50 nations. The average score of U.S. students was 8% above the average of all tested nations.[196]

* In reading literacy tests administered by the Program for International Student Assessment to 15-year-old students during 2018, U.S. students ranked 9th among 36 developed nations. The average score of U.S. students was 4% above the average of all tested nations.[197] [198] [199]

* U.S. students outperformed Canada and New Zealand on the 4th-grade reading exam but underperformed them on the 15-year-old reading exam. U.S. students moved ahead of Hungary, Latvia, Norway, and the United Kingdom between the 4th grade and 15 years old.[200] [201]

* In 2013, Randi Weingarten, president of the American Federation of Teachers labor union, stated:

* In 2013, the U.S. ranked 5th among 33 developed nations in average spending per full-time K–12 student. The average spending per U.S. student was 28% above the average of these nations, and U.S. 15-year-olds ranked 19th in reading and 30th in math.[203] [204] [205]

* Among the same nations, U.S. 15-year-olds did not match or outperform any nation in both reading and math that outspent the U.S. The following nations matched or outperformed the U.S. in both reading and math while spending less than the U.S.:

|

Nation |

U.S. Spending Premium |

Math Advantage Over U.S. |

Reading Advantage Over U.S. |

|

Belgium |

2% |

8% |

0% |

|

United Kingdom |

3% |

5% |

0% |

|

Denmark |

6% |

9% |

1% |

|

Sweden |

9% |

5% |

1% |

|

Netherlands |

12% |

9% |

1% |

|

Germany |

15% |

8% |

2% |

|

France |

22% |

5% |

0% |

|

Finland |

24% |

9% |

6% |

|

Japan |

24% |

13% |

4% |

|

Australia |

25% |

5% |

1% |

|

Ireland |

27% |

7% |

5% |

|

New Zealand |

32% |

5% |

2% |

|

Slovenia |

33% |

9% |

2% |

|

Portugal |

35% |

5% |

0% |

|

South Korea |

42% |

12% |

4% |

|

Spain |

53% |

3% |

0% |

|

Estonia |

75% |

11% |

4% |

|

Poland |

78% |

7% |

2% |

* In 1885, the Jersey City, NJ school district spent an average of $13.24 over the course of the year for each of the 14,926 students in average daily attendance.[209] Adjusted for inflation into 2021 dollars, this is an average of $399 per student per year, or 1/43 the national average spending per student in 2020.[210] [211]

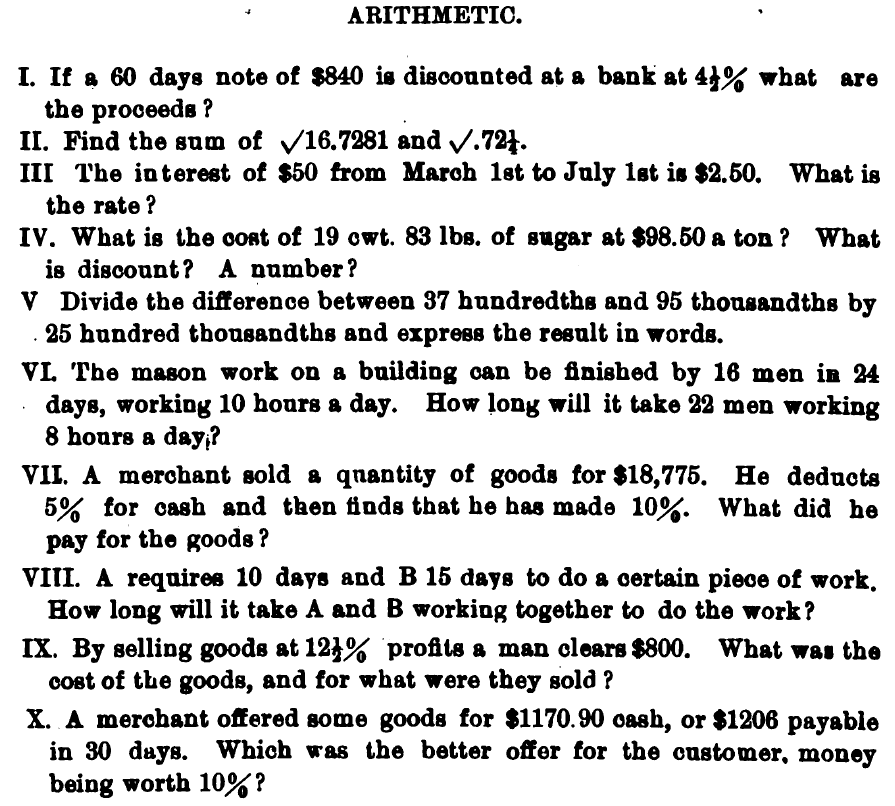

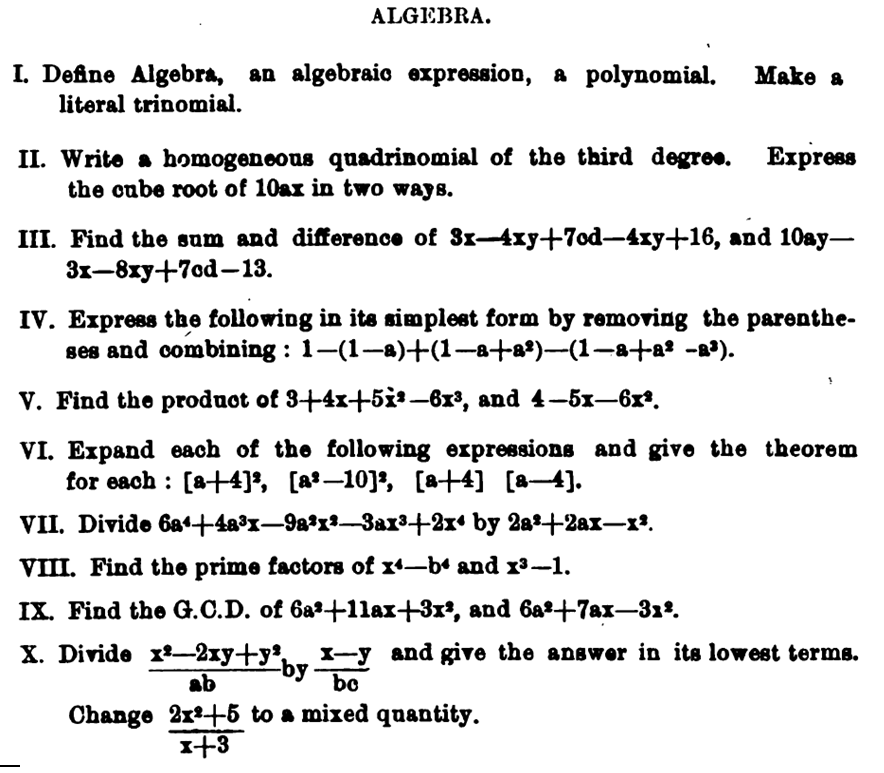

* Below are the arithmetic and algebra questions from the 1885 high school entrance exam in Jersey City, NJ. In order to enter high school, students had to score at least 75%. A copy of the full test and the names and scores of all passing students are shown in this footnote.[212]

Arithmetic

Algebra

* In the 2020–21 school year, public 4-year colleges spent an average of $52,896 per full-time-equivalent student. For other types of colleges, spending per student varied as follows:

|

Control of Institution[213] |

4-Year Colleges |

2-Year Colleges |

|

Public |

$52,896 |

$21,729 |

|

Private Nonprofit |

$69,145 |

$27,464 |

|

Private For-Profit |

$17,661 |

$14,828 |

* From 2000 to 2021, the average inflation-adjusted spending by private non-profit 4-year colleges per full-time-equivalent student rose by 29%. For other types of colleges, spending per student varied as follows:

* In the 2020–21 school year, private for-profit colleges spent an average of 28% of their finances on student instruction. For all types of colleges, their breakdown of spending on various functions varied as follows:

|

Function |

Public |

Private Nonprofit |

Private For-Profit |

|

Instruction[216] |

27% |

29% |

28% |

|

Research[217] |

10% |

11% |

0.2% |

|

Public service[218] |

4% |

1% |

|

|

Academic support[219] |

8% |

9% |

65% |

|

Student services[220] |

5% |

8% |

|

|

Institutional support[221] |

9% |

13% |

|

|

Hospitals[222] |

15% |

16% |

|

|

Auxiliary enterprises[223] |

7% |

7% |

2% |

|

13% |

6% |

6% |

* During 2021, federal, state and local governments spent $232 billion on higher education.[228] not including additional government funding of university research, university hospitals, and student loans.[229] [230] [231] This $232 billion amounts to:

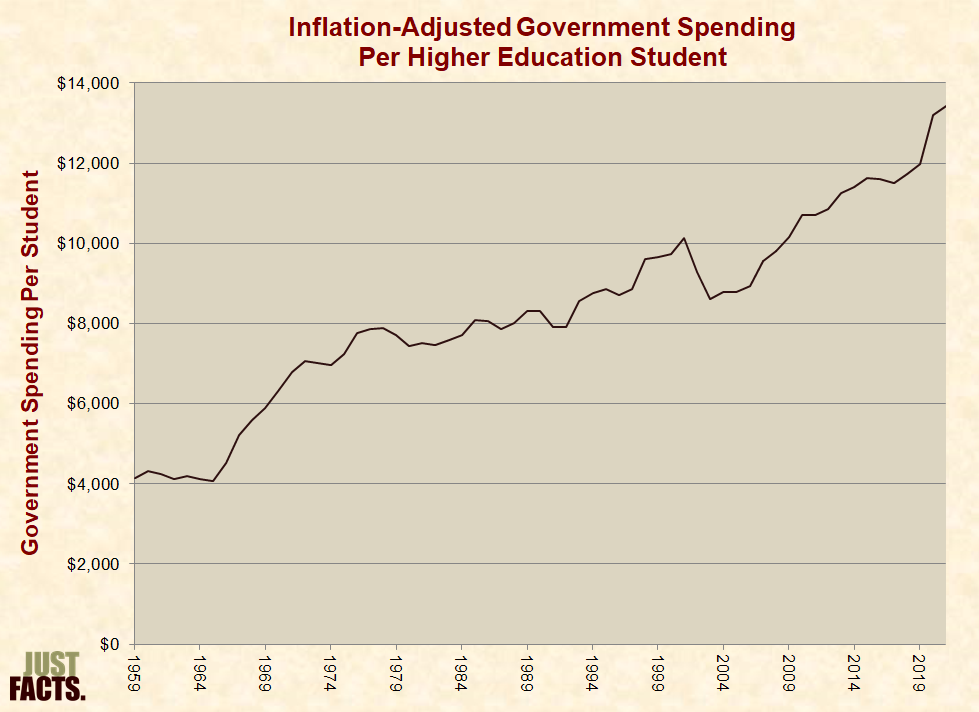

* From 1959 to 2021, inflation-adjusted government spending on higher education rose from $4,137 per student per year to $13,434. This doesn’t include additional government funding for university research, university hospitals, and student loans:

* Colleges and universities publish “rates” or “sticker prices” for their tuition, fees, room, and board. Individual students pay less than these sticker prices if they receive discounts, scholarships, or financial aid.[242]

* In the 2020–21 school year, the average sticker price for:

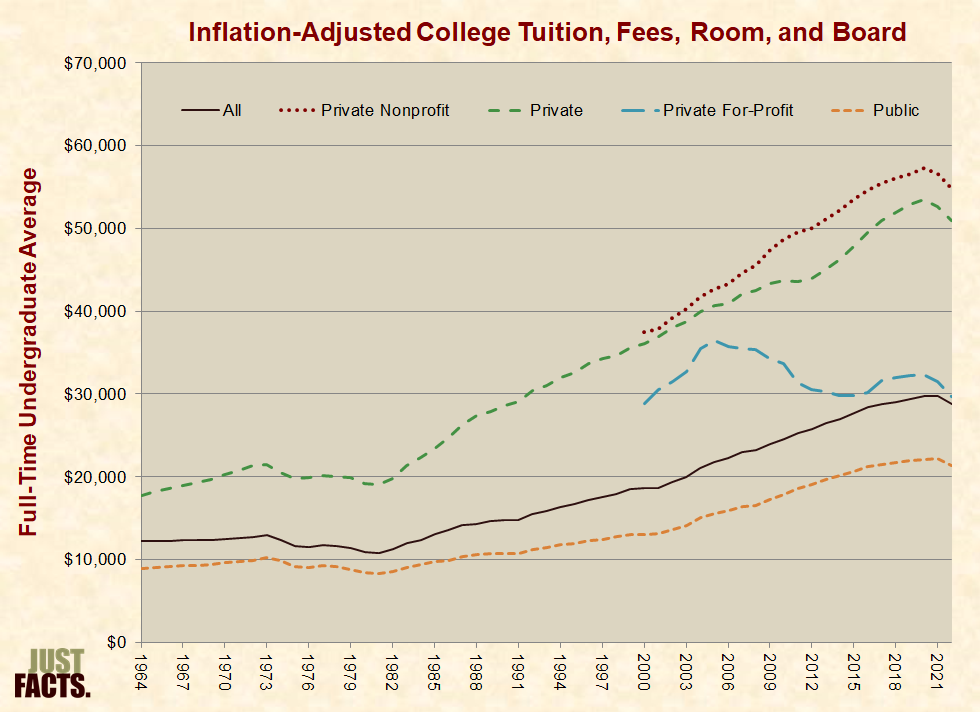

* From 1964 to 1980, the average annual inflation-adjusted sticker price for tuition, fees, room, and board for all full-time undergraduate students fell by 11%. From 1980 to 2022, it rose by 167%:

* Colleges that are subsidized by taxpayers and donors generally spend more money per student than their sticker prices. In the 2020–21 school year, the average amount spent by colleges for each full-time-equivalent student at:

* For the 2012 tax year, 12.2 million tax filers (claiming 13.4 million students) received $19 billion in higher education tax credits.[250] Tax credits decrease the taxes that people must pay on a dollar-for-dollar basis, and some are refundable, which means that households with credits that exceed their income taxes receive the difference as cash payouts from the government. Per the IRS Inspector General, “the risk of fraud for these types of claims is significant.”[251] [252] [253] [254] [255]

* In 2015, the IRS Inspector General published an investigation of higher education tax credits for the 2012 tax year. The investigation found that 3.6 million tax filers (claiming 3.8 million students) received $5.6 billion in credits “that appear to be erroneous based on IRS records.” Some examples include:

* The federal government offers student loans that can be used to attend college, vocational schools, or trade schools.[257]

* There are different types of federal student loans, each with its own set of conditions and interest rates. Most of these loans generally require borrowers to pay back the money within 10 years of finishing college.[258]

* For people with good credit histories, the market rates on private student loans are sometimes lower than the rates on federal student loans.[259]

* As of the first quarter of 2023:

* In the context of student loans:

* In the first quarter of 2023, 1% of all federal student loans were actively being repaid. The other 99% fell into the following categories:

* Per the U.S. Treasury, the federal government creates loan programs so that people who are “unable to afford credit at the market rate” or have a “high risk” of defaulting can borrow money at “an interest rate lower than the market rate.”[272]

* Per the U.S. Congressional Budget Office, “When the government extends credit, the associated market risk of those obligations is effectively passed along to citizens….”[273]

* Per a 2014 report by the U.S. Treasury Borrowing Advisory Committee:

* Per Deborah J. Lucas, director of the MIT Center for Finance and Policy and former chief economist of the Congressional Budget Office:[275]

* In 1965, the 89th U.S. Congress and Democratic President Lyndon B. Johnson created a program to finance student loans for higher education. These loans were issued by private lenders and guaranteed against default by the federal government.[277] [278] [279]

* In 1993, the 103rd U.S. Congress and Democratic President Bill Clinton created a program to finance student loans directly from the U.S. Treasury. The law required that increasing portions of all new federal student loans be made through this program.[280] The bill passed Congress with 85% of Democrats voting for it and 100% of Republicans voting against it.[281]

* In 2010, the 111th Congress and Democratic President Barack Obama passed a law requiring that all new federal student loans be financed directly from the U.S. Treasury.[282] [283] [284] The bill passed Congress with 88% of Democrats voting for it and 99% of Republicans voting against it.[285]

* As of September 30th, 2022, 93% of all student loans were owed to or guaranteed by the federal government.[286]

* As of first quarter of 2023, Americans had $1.6 trillion of outstanding student loan debt:

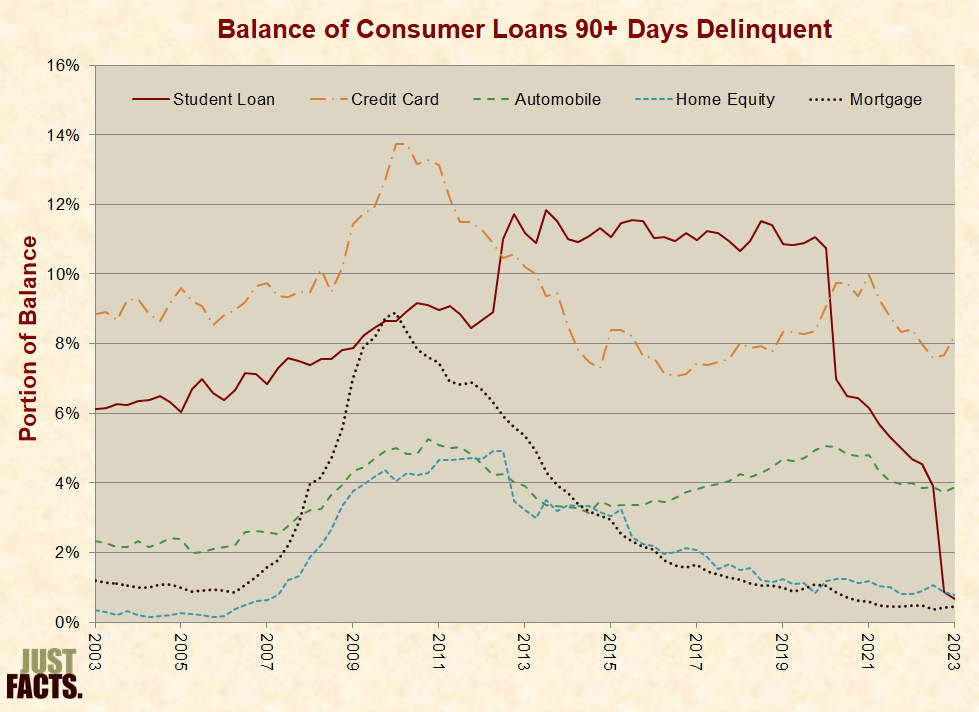

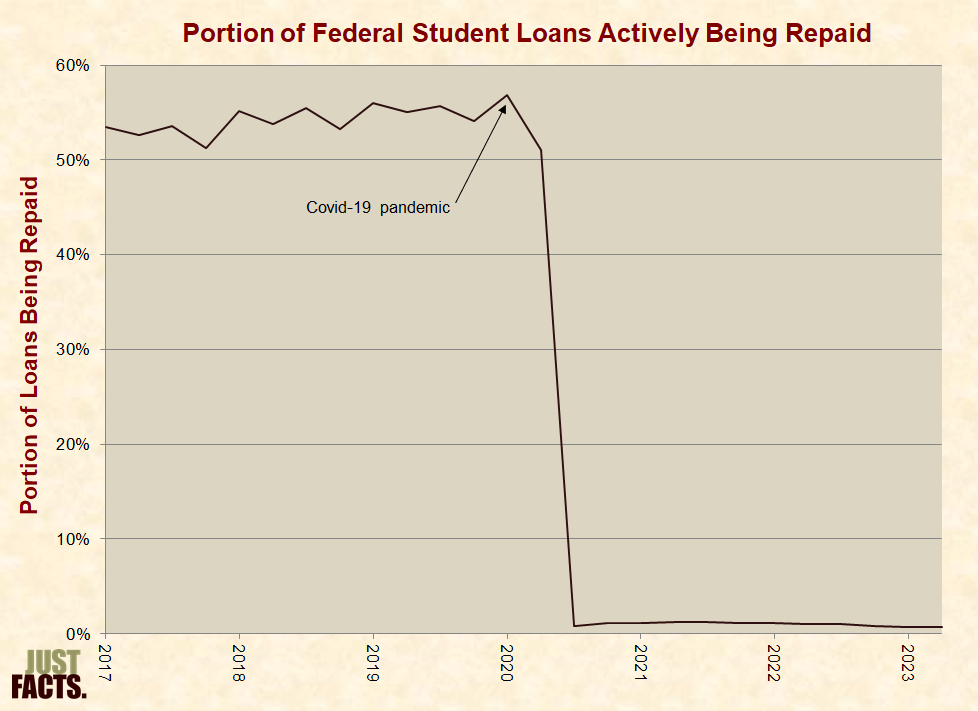

* In 2012, the 90+ day delinquency rate for student loans exceeded that of credit cards for the first time since reliable data on this measure became available in 2003.[291] It remained the most common type of delinquent debt until early 2020 when the federal government passed a law that suspended student loan payments in the wake of the Covid-19 pandemic:[292] [293] [294] [295] [296]

* In 2020, Congress passed and President Trump signed a “Covid-19 relief” law that suspended student loan payments and interest through September 2020.[301] After this, President Trump and President Biden repeatedly extended this policy without clear legal authority to do so.[302] The cost to taxpayers of these actions was roughly $102 billion.[303]

* Before student loan payments were suspended in 2020, 57% of all federal student loan balances were actively being repaid or less than 360 days delinquent. As of second quarter of 2022, this figure is 1%:

* Before the federal government suspended student loan payments,[307] the 43% of loans that were not actively being repaid fell into the following categories:

* When people don’t pay back student loans because politicians forgive them, this debt is transferred to people who did not borrow the money.[310] [311]

* Since 1976, federal law has prohibited people from reneging on federal student loans by filing for bankruptcy (except in rare cases).[312] [313] [314] [315]

* Federal laws authorize more than 50 federal student loan forgiveness and repayment programs. Such programs reduce or eliminate student loan debt for various reasons, such as having income below certain thresholds or being a government employee.[316]

* In 2015, President Obama instructed his administration to “develop recommendations for regulatory and legislative changes for all student loan borrowers, including possible changes to the treatment of loans in bankruptcy proceedings….”[317]

* In 2015, the Obama administration issued regulations that limited student loan payments to 10% of borrowers’ monthly incomes and forgave:

* In 2021–22, the Biden administration issued regulations that:

* By law, the U.S. Department of Education can forgive federal student loans for borrowers who attended a school that “violated state law” through “misleading activities or other misconduct [that] directly relate to the loan or to the educational services for which the loan was provided.”[323] The Obama administration in 2015 and Biden administration in 2021–22 announced regulations to “streamline” these applications and expand the scope of loan forgiveness to include:

* With regard to this law:

* In 2022, President Biden announced that he is “forgiving” $20,000 of student loan debt for the vast bulk of Pell Grant recipients and $10,000 for others who owe student loans.[343] With regard to this action, the Biden administration:

* The Penn Wharton Budget Model estimated that Biden’s student loan cancellations and payment reductions would have cost $605 billion to more than $1 trillion.[348] If these expenses were equally divided among all households in the U.S., they would have cost each household about $4,700 to $7,700.[349]

* With regard to the legality of Biden’s action:

* Shortly after the Supreme Court’s ruling, the Biden administration:

* In total, the Biden administration cancelled $117 billion in student loans from 2021–23, including:

* To receive a federal student loan to attend a specific college, the college must be accredited. This means that it must be officially certified as an institution that delivers quality education.[365]

* The process of accreditation takes place at least once every 10 years and is generally conducted by private non-profit agencies. These agencies are sanctioned by the Department of Education, which is under the authority of the U.S. president.[366] [367]

* Accrediting agencies have the power to sanction colleges by denying, suspending, or revoking their accreditation. These agencies can also take interim actions, such as placing colleges on probation and requiring them to submit financial reports.[368]

* In January 2015, the U.S. Government Accountability Office published the results of an investigation of accrediting agencies and the Department of Education from October 2009 through March 2014. The study found that:

* Per the study’s conclusion:

* Five months after the results of this investigation were published, the Obama administration issued a press release stating:

* When the federal government lends money for student loans, the government doesn’t report these amounts as outlays in the federal budget. Instead, the budget reflects only what the government projects it will lose or gain on these loans.[372] [373]

* Under federal budget rules, the federal government typically projects that it will make money on student loans. Thus, the more money the government loans, the better the budget appears to be.[374]

* Federal budget rules do not account for the market risk of issuing student loans. Market risk stems from the possibility that the economy will perform worse than the government projects, which would increase default rates and have other negative effects on returns from these loans.[375] [376]

* Per estimates made by the Congressional Budget Office:

* In 2022, the U.S. Government Accountability Office reported:

* Institutes of higher learning are also known as colleges, universities, and post-secondary schools.[380] Such institutions award:

* As of the fall of 2021, roughly 19.0 million students were attending U.S. colleges. Among these students:

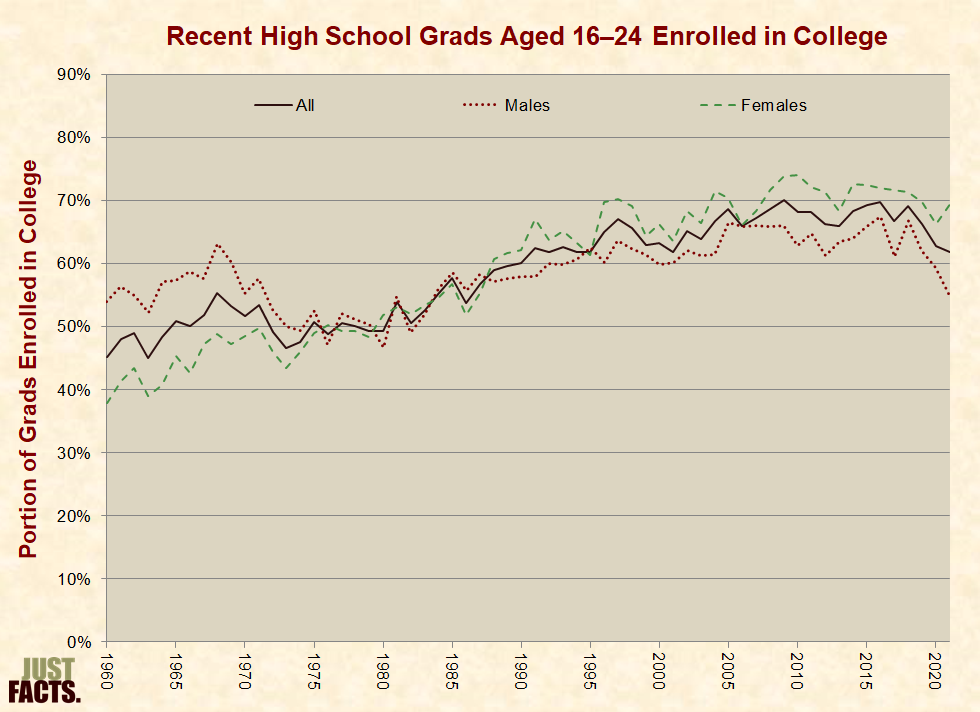

* From 1960 to 2021, the portion of recent high school graduates (aged 16–24) enrolled in college:

* Among recent high school graduates of different racial/ethnic groups, the rates of college enrollment in 2021 were:

* Among full-time, new college students who entered a 2-year college in 2017, 34% graduated from it within 150% of the normal time required to do so (typically three years). This was true for:

* Among full-time, new college students who entered a 4-year college in 2014, 47% graduated from the same institution within four years.[393]

* Among full-time, new college students who entered a 4-year college in 2013, 63% graduated from it within six years. This was true for:

* In 2021, people aged 25–64:

* Click here for more data on education and earnings.

* From 1961 to 2003, the average time spent by full-time college students on educational activities like attending class and studying dropped from roughly 40 hours per week to 27 hours per week.[397]

* During the 2005–06 and 2006–07 school years, full-time students at 4-year colleges spent an average of about:

• 27–28 hours per week or 16–17% of their time on educational activities.

• 43 hours per week or 26% of their time on leisure activities and sports.[398]

* In 1960, roughly 15% of college course grades were A’s. By 1988, approximately 31% of grades were A’s. By 2013, about 45% of grades were A’s.[399] [400]

* The Collegiate Learning Assessment (CLA) is a test designed to measure the “core outcomes” of higher education, including “critical thinking, analytical reasoning, problem solving, and writing.”[401] This assessment evaluates how well college students perform “real-world tasks that are holistic and drawn from life situations.”[402] [403]

* In 2014, Professor Richard Arum of New York University and Assistant Professor Josipa Roksa of the University of Virginia published a study using the CLA to measure the “critical thinking, complex reasoning, and writing skills” of 1,666 full-time students who entered 4-year colleges in the fall of 2005 and graduated in the spring of 2009. The authors found that:

* Using test questions from the National Center for Education Statistics’ adult test of practical literacy, the American Institutes for Research assessed the literacy skills of 1,827 graduating college students in 2003. These students were randomly selected from across the U.S., and each was graded as Proficient, Intermediate, Basic, or Below Basic on three different types of literacy:[406]

1) Prose Literacy, which is the ability to “search, comprehend, and use information from continuous texts,” such as “editorials, news stories, brochures, and instructional materials.” Students who were proficient in this included:

2) Document Literacy, which is the ability to “search, comprehend, and use information from noncontinuous texts,” such as “job applications, payroll forms, transportation schedules, maps, tables, and drug or food labels.” Students who were proficient in this included:

3) Quantitative Literacy, which is the ability to “identify and perform computations … using numbers embedded in printed materials,” such as “balancing a checkbook, figuring out a tip, completing an order form, or determining the amount of interest on a loan from an advertisement.” Students who were proficient in this included:

* The study also found:

* A 2013 Gallup poll of 623 business leaders found that over two-thirds do not think U.S. college graduates have the necessary “skills and competencies” for their particular business.[412]

* In 2020, the Association of American Colleges and Universities commissioned a poll of employers who hire people with bachelor’s degrees to assess their views of recent college graduates. The poll included 496 employers, had a margin of sampling error of plus or minus 5 percentage points, and found the following results:

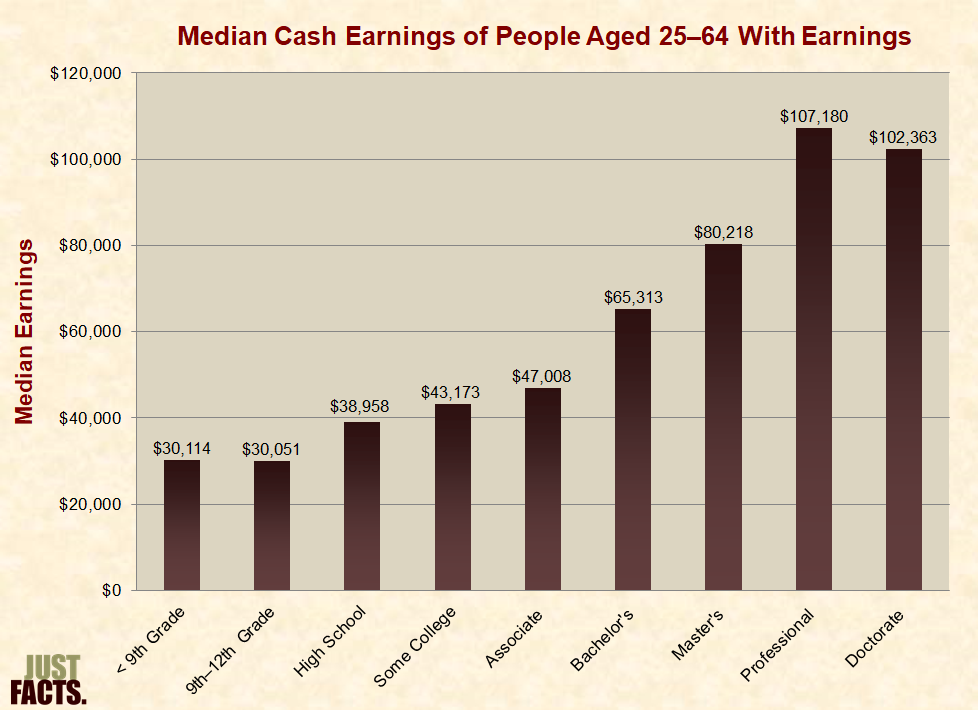

* In 2021, U.S. residents aged 25 to 64 reported average cash earnings of $54,252.[415] Cash earnings do not include non-cash compensation, such as employee fringe benefits.[416] For varying levels of education, average reported cash earnings were as follows:

* In 2021, 79% of U.S. residents aged 25–64 reported at least some cash earnings and 21% did not report any cash earnings. For varying levels of education, the rates were as follows:

* Among U.S. residents aged 25–64 who reported cash earnings in 2021, average cash earnings were $68,900. Among these same people, median cash earnings were $51,000.[421] For varying levels of education, median cash earnings were as follows:

* During 2022, private consumers and nonprofit organizations in the U.S. spent $22.0 billion on day care and preschools/nursery schools.[424] [425] [426] [427] [428]

* During 2015, the federal government funded 47 programs that provided or subsidized education and/or childcare for children under the age of five.[429]

* The largest federal education/childcare program for preschoolers is called “Head Start.”[430] [431] During 2022, Head Start served 788,341 children and 12,736 pregnant women at some point during the year.[432]

* In 2021, the federal government spent an average of $12,809 for each person enrolled in Head Start. This does not include additional funds from state governments.[433]

* Federal law requires that at least 90% of Head Start enrollees have incomes below 130% of the federal poverty line. To determine if the law was being enforced, the U.S. Government Accountability Office (GAO) conducted 15 undercover tests of Head Start centers in six states from 2008 to 2010. The investigation found the following:

* From 2017 to 2019, GAO reviewed the Head Start program to determine if eligibility and enrollment problems persisted. Of the 15 centers covertly tested:

* During 2021, 26% of all 3-to-4 year-olds in the U.S. were enrolled in government-controlled education programs. In 1965, this figure was 1%.[436]

* During 2021, 19% of all 3-to-4 year-olds in the U.S. were enrolled in private education programs. In 1965, this figure was 4%.[437]

* In 2013, President Obama called on Congress to fund certain initiatives that would allow every child in the U.S. from birth to age five to have access to government-controlled early learning programs. Specifically, he called for funding to:

* In May 2015, U.S. Senator Patty Murray (D-WA) introduced a bill that would enact much of President Obama’s early learning agenda. At the end of President Obama’s term in January 2017:

* In 2021, President Biden proposed a social spending plan that called for:

* In September 2021, U.S. Representative John Yarmuth (D-KY) introduced a bill that would have enacted much of President Biden’s childcare and preschool agenda.[447] The bill passed the House of Representatives with 220 of 221 Democrats voting for it and 212 of 213 Republicans voting against it.[448] The Democrat-controlled Senate however, stripped Biden’s childcare and preschool agenda from the bill.[449] [450] [451]

* The largest federal education/childcare program for preschoolers is Head Start, which “provides comprehensive educational, social, health, and nutritional services to low-income preschool children and their families.”[452] [453] [454] [455] [456]

* Head Start operates mostly during the school year and has full-day and part-day programs. When Head Start programs are in session, the average participant attends about 24 to 28 hours per week.[457] [458]

* From 2002 through 2008, the U.S. Department of Health & Human Services conducted a nationally representative study of 3- and 4-year-old children whose parents had applied for enrollment in Head Start and were found to be eligible. The study included 4,667 children from high-poverty communities. The design and results were as follows:

* In 2022, the Inspector General of the U.S. Department of Health & Human Services published a five-year review of the Head Start program that found 27% of grant recipients failed to promptly report incidents of child neglect, including:

* In 2022, Vanderbilt University conducted an experimental study of two groups of 4-year children whose parents applied for enrollment in a government preschool program in Tennessee. The study included 2,990 children from low-income families. The design and results were as follows:

* From 1962 to 1967, a Ph.D. public school administrator named David Weikart led a study of 123 preschool-aged children in a town near Detroit named Ypsilanti, Michigan. This famous study is known as the “High/Scope Perry Preschool” study, because HighScope is the name of the research firm that Weikart later founded, and the study was conducted on children who lived near the Perry Elementary School in Ypsilanti.[463] [464] [465] [466]

* The study’s design was as follows:

* The authors of a 2008 paper in the Journal of the American Statistical Association examined the outcomes of the four Perry sample groups and found the following statistically significant outcomes at different ages.

* The authors of the study also found:

* Using “novel statistical approaches” to account for “small sample sizes” and a “corrupted randomization” process in the original study, researchers at the University of Chicago found several other statistically significant outcomes between the four Perry sample groups at different ages. For example:

* Given the sample sizes of the four Perry groups (roughly 25 each), the approximate margin of error with 95% confidence for any outcome is ± 20 percentage points.[492] [493] Per an academic textbook on statistical analysis by University of Pennsylvania professor Paul D. Allison:

* Policymakers and activists have pointed to the Perry program as a reason to enact universal government preschool.[495] [496] [497] [498] [499] [500] Per an academic book on applied statistics by Harvard Ph.D. and social physiologist Rebecca M. Warner:

* The subjects of the Perry study (black, impoverished, IQ of 70–85) represented 2% of the U.S. population and 16% of the African American population at the time the study was conducted.[503] [504]

* From 1972 to 1977, researchers at the University of North Carolina led a study of 111 preschool-aged children in the area of Chapel Hill, NC. This study is known as the “Abecedarian Project,” because that was the name of the main curriculum used in the program.[505] [506] [507]

* The study’s design was as follows:

* The authors of a 2008 paper in the Journal of the American Statistical Association examined the outcomes of the four Abecedarian sample groups and found the following statistically significant outcomes at different ages:

* The authors of the study also found:

* Policymakers and activists have cited the Abecedarian Project as a reason to enact universal government preschool.[528] [529]

* Laws in all 50 U.S. states generally compel people to:

* School choice initiatives allow parents to select the schools their children attend, with part or all of the costs paid by their taxes or other government revenues. This can include:

* In the U.S., government revenues regularly fund the education of students who attend private colleges and universities but rarely students who attend private K–12 schools.[540] [541] [542]

* In other economically advanced nations—like Austria, Canada, Spain, France, Hungary, Australia, New Zealand, and the Netherlands—government revenues commonly fund the education of students who attend private K–12 schools and sometimes those who are homeschooled.[543]

* In different nations, governments exercise varying amounts of centralized control over public and private schools. Public schools in some countries have more autonomy than private schools in others.[544]

* Per the academic serial work Handbook of Research on School Choice:

* In the 2019–20 school year, governments in the U.S. spent an average of $17,013 for every student enrolled in K–12 public schools.[550] [551] This excludes state administration spending, unfunded pension liabilities, and non-pension post-employment benefits.[552]

* In the 2019–20 school year, the average spending per student enrolled in private K–12 schools was about $9,709.[553] [554] [555] [556] [557] [558]

* Per the academic textbook Antitrust Law:

* Per the U.S. Supreme Court’s unanimous decision in Abood v. Detroit Board of Education:

* Governments are subject to certain types of competition, because people and businesses sometimes migrate to locations where governments provide better value for their tax dollars, and because voters sometimes remove politicians for reasons such as increasing taxes and government spending.[564] [565]

NOTE: In order to curb the methodological trickery that besets public policy debates, Just Facts has developed Standards of Credibility that call for the presentation of “data in its rawest comprehensible form.” However, the results of all experimental studies on the academic outcomes of students who experience school choice are more processed than Just Facts would prefer. Thus, instead of ignoring them or attempting to analyze all of the raw data, Just Facts has briefly summarized all of these studies and documented their results in the footnotes below.

* At least 23 experimental (or quasi-experimental) studies have been conducted on the academic outcomes of students who experience school choice.[566] [567] Among them:

* In a 2014 interview, Bill O’Reilly asked Barack Obama, “Why do you oppose school vouchers when it would give poor people a chance to go to better schools?” Obama replied:

* A 2010 experimental study of a school voucher initiative in the District of Columbia published by the Obama administration’s Department of Education found the following statistically significant results:

* Per a 2004 report by the Civil Rights Project at Harvard University, the Urban Institute, Advocates for Children of New York, and the Civil Society Institute:

* The 2012 Democratic Party Platform states:

* In 2013, the Journal of Policy Analysis and Management published an experimental study of the same District of Columbia voucher initiative by the same lead author. The study found the following statistically significant results:

* In 2011, the Quarterly Journal of Economics published an experimental study of a public school choice initiative in the 20th largest school district in the nation (Charlotte-Mecklenburg, North Carolina). The study compared the adult crime outcomes of male students who won and did not win a lottery for their parents’ first choice of school. The author found the following statistically significant results:

* Per a 2006 book about school choice written by Harvard professors William G. Howell and Paul E. Peterson:

* The primary measure of school resources is spending per student.[598] [599] [600]

* School choice initiatives that allow students to attend private schools typically increase the funding per student in public schools, because public schools do not have to educate students who leave and because private schools typically spend less per student than public schools.[601] [602]

* Certain school costs are fixed in the short term (like buildings), and thus, the cost savings of educating fewer students occurs in steps instead of linearly. This means that private school choice programs can temporarily decrease the funding per student in public schools.[603]

* In 2022, the journal Education Next published a study of a Florida school choice initiative that awards scholarships for low-income students to use towards private school tuition and transportation. It measured how “increased competition” from the program’s expansion since 2002 affected educational and behavioral outcomes of students who remained in public schools. The study found that increased program enrollment and competition:

* In 2013, the Journal of School Choice: International Research and Reform published a systematic review of 21 “high-quality” studies about the academic outcomes of U.S. students who remain in public schools after other students leave through choice programs. This review was designed to measure the effects of competition on public schools whose enrollments are threatened by private school choice programs. The author found:

* In 2004, the journal Education Next published an experimental study of a Florida school choice initiative that offered private and public school vouchers to students enrolled in chronically failing public schools. The study compared the academic gains of public school students whose schools were eligible for vouchers and public school students whose schools were not eligible for vouchers. The study found the following statistically significant results:

* According to donations reported to the Federal Election Commission, the following education groups were among the top 100 organizations that gave the most money to federal candidates, parties, political action committees, and related organizations during the 1990–2022 election cycles:

|

Group |

Rank in the Top 100 |

Total Contributions |

Portion to Democrats & Liberal Groups |

|

American Federation of Teachers (AFT) |

16 |

$127,218,032 |

100% |

|

National Education Association (NEA) |

20 |

$108,586,479 |

96% |

* The NEA and AFT are labor unions.[610] For facts about the accuracy of union donations reported to the Federal Election Commission, visit Just Facts’ research on labor unions.

* In 2009, the president of the NEA sent an open letter to Democrats in the U.S. House and Senate stating that “opposition to [private school] vouchers is a top priority for NEA.”[611]

* The 2020 Democratic Party Platform opposes private school vouchers and supports a ban on federal funding of for-profit charter schools.[612]

* The Republicans didn’t adopt a platform in 2020.[613] The 2016 Republican Party Platform supports “options for learning, including home-schooling, career and technical education, private or parochial schools, magnet schools, charter schools, online learning, and early-college high schools,” as well as “education savings accounts (ESAs), vouchers, and tuition tax credits.”[614]

* The President of the United States appoints justices to the U.S. Supreme Court. These appointments must be approved by a majority of the Senate.[615]

* Once seated, federal judges serve for life unless they voluntarily resign or are removed through impeachment, which requires a majority vote of the House of Representatives and two-thirds of the Senate.[616]

* Senate rules previously allowed for a “filibuster,” in which a vote to approve a judge or Supreme Court justice could be blocked unless a super-majority of the senators (typically 60 out of 100) agreed to let it take place.[617] [618] [619] These rules were repealed:

* Once seated, federal judges serve for life unless they voluntarily resign or are removed through impeachment, which requires a majority vote of the House of Representatives and a two-thirds majority vote in the Senate.[622]

* In 2002, the U.S. Supreme Court ruled (5 to 4) that a school choice initiative in Cleveland was constitutional (details below). Five of the seven justices appointed by Republicans ruled that it was constitutional, and both of the justices appointed by Democrats ruled that it was not.[623]

* A nationally representative poll of U.S. adults commissioned in 2015 by Education Next and the Kennedy School of Government at Harvard University found that the following portions of Americans:

* An analysis of U.S. Census data from the year 2000 by the Thomas B. Fordham Institute (a proponent of school choice) found that the following portions of parents were sending at least one of their own children to a private K–12 school:

* The following opponents of private school choice personally attended and/or sent their own children to private K–12 schools:

* The American Civil Liberties Union (ACLU) opposes taxpayer-funded private school choice programs. One of the ACLU’s arguments for this stance is that:

* The ACLU supports taxpayer-funded abortions. With regard to whether all taxpayers should be forced to support practices with which they may strongly disagree, the ACLU asks the following rhetorical question:

And answers:

* Per the academic serial work Handbook of Research on School Choice:

* Per the academic reference book 21st Century Geography, “economically depressed populations with limited access to resources … have restricted choices on where they can live….”[665]

* In 2013, homes in top-ranked school districts cost an average of $50 more per square foot than homes in average-ranked school districts.[666]

* In 2009, Barack Obama’s Secretary of Education, Arne Duncan, was asked, “Where does your daughter go to school, and how important was the school district in your decision about where to live?” Duncan replied:

* In 2009, families living in Arlington, Virginia reported an inflation-adjusted median cash income of $193,467 the highest among all counties in the United States.[668] [669]

* When Arne Duncan was the chief executive of the Chicago public school system, his office contacted school principals to help the children of politically connected parents get into better public schools. Per a 2010 Chicago Tribune article:

* In the 2002 case of Zelman v. Simmons-Harris, the U.S. Supreme Court ruled (5–4) that a school choice initiative in Cleveland was constitutional. This program provided tuition aid for students:

* The Zelman case hinged upon:

* Per the majority ruling in Zelman:

* Per a dissent by Justice David Souter:

* Per a concurrence by Justice Sandra Day O’Connor, the Cleveland school choice program:

* Per a dissent by Justice John Paul Stevens:

* Per a concurrence by Justice Clarence Thomas, the Cleveland program:

* State supreme courts have ruled differently regarding whether various school choice programs are prohibited by their respective constitutions.[680] For example, the states of Florida and Indiana both enacted school choice programs that allowed certain children to attend private schools, but:

Espinoza v. Montana Department of Revenue

* In the 2020 case of Espinoza v. Montana Department of Revenue, the U.S. Supreme Court ruled (5–4) that a publicly subsidized scholarship program could not exclude religious schools.[683]

* The Espinoza case hinged upon:

* Per the majority ruling in Espinoza:

* Per a dissent by Justice Sonia Sotomayor:

* Per a concurrence by Justice Clarence Thomas:

* Per a dissent by Justice Stephen Breyer:

* Per a concurrence by Justice Samuel Alito:

* As of 2023, the Friedman Foundation for Educational Choice has identified 81 school choice programs in 33 states, the District of Columbia, and Puerto Rico.[691]

* Per the official Common Core website:

* The Common Core standards were developed and are maintained by the Common Core State Standards Initiative (CCSSI), which is a joint project of the Council of Chief State School Officers and the National Governors Association’s Center for Best Practices.[693] [694] [695]

* The Council of Chief State School Officers is a nonprofit organization controlled by the chief public education officials of each state, the District of Columbia, the U.S. military, and each U.S. territory.[696]

* The National Governors Association is an organization funded by the states and controlled by the governors of 55 U.S. states, territories, and commonwealths.[697] [698] The Center for Best Practices is a nonprofit organization that is “an integral part of the National Governors Association” but is “funded through federal grants and contracts, fee-for-service programs, private and corporate foundation contributions, and NGA’s Corporate Fellows program.”[699] [700]

* The Bill and Melinda Gates Foundation provided most of the money to create Common Core. This included money to develop the standards and build support for Common Core through donations to politicians, unions, civic leaders, and business organizations. Bill Gates, the wealthiest person in the world at the time, personally authorized this funding.[701] [702]

* In July 2009, CCSSI announced the names of 29 people that it had chosen to write the Common Core standards. The press release stated that:

* In September 2009, CCSSI announced that six governors and six chief state school officers had appointed a 29-person “validation committee” of education experts to review and certify the Common Core standards.[704]

* As a condition of being on the validation committee, each member had to agree to keep all “deliberations, discussions, and work” of the committee “strictly confidential” in perpetuity.[705] [706]

* In June 2010, the validation committee issued a report certifying the standards. The report listed 24 people who had signed the standards and:

* At least two of the committee members who declined to certify the standards have publicly criticized them and the process by which they were created.[710] [711]

* In November 2009, the Obama administration issued regulations governing how states could compete for $4.35 billion in federal education funds under its “Race to the Top” program. These regulations required states to demonstrate their “commitment to adopting a common set” of K–12 education standards. The regulations also stipulated that states would earn “high points” if they adopted the same standards as the “majority of the States in the country.”[712] [713] [714] [715]

* By September 2011, 44 states and the District of Columbia had adopted the Common Core standards.[716] [717]

* Among the 46 states that had adopted all or part of the Common Core standards by early 2014, six had done so by legislative action, and 40 by decisions made by state boards of education or chief education officials.[718] [719]

* As of March 2019:

* New Hampshire, which retains the Common Core standards, passed a law in 2017 that prevents the state government “from requiring the implementation of the Common Core standards in any school or school district in this state.[721]

* In 2020, the governor of Florida removed and replaced the Common Core standards.[722]

* CCSSI asserts that the Common Core standards:

* Two of the Common Core validation committee members who refused to validate the standards assert that they:

* Organizations other than CCSSI are developing common standards for science, world languages, and arts.[730]

* In the field of education, “centralization” refers to the transfer of decision-making authority from individuals, teachers, schools, and local governments to state or national governments. “Decentralization” is the opposite of centralization.[731] [732]

* Common Core is a form of educational centralization because it specifies “a single body of knowledge and skills that students … will be expected to possess.”[733]

* The alleged benefits of centralizing education include but are not limited to:

* The alleged benefits of decentralizing education include but are not limited to:

* Some of the factors that make it difficult to determine the effects of centralization and decentralization include:

* CCSSI asserts that a “root cause” of U.S. academic stagnation has been “an uneven patchwork of academic standards that vary from state to state and do not agree on what students should know and be able to do at each grade level.”[768]

* In October 2015, Just Facts asked CCSSI to provide “specific studies” that prove academic stagnation has been caused by differing state education standards.[769] CCSSI responded but did not provide such research.[770]

* From 1920 to 2020, the portion of K–12 public school funding provided by:

* As the federal and state governments have funded a growing share of K–12 school expenses, the U.S. education system has become increasingly centralized. This has transferred decision-making power from community schools to higher levels of government through:

* Per a 1980 academic book on the U.S. education system:

* Per a 1997 academic book on education decentralization:

* The complete Common Core math standards are available here.[789]

* R. James Milgram, Emeritus Professor at Stanford University’s Department of Mathematics, was the only mathematician who served on Common Core’s validation committee.[790] [791] [792] He refused to certify the standards and has been critical of them.[793]

* Other mathematicians have supported and opposed the standards.[794] [795] [796]

* CCSSI asserts that the math standards “call for speed and accuracy in calculation.”[797]

* The math standards require first graders to “think of whole numbers between 10 and 100 in terms of tens and ones” and solve problems such as:

* The math techniques above are illustrated in the following videos produced by a local NBC television station. The station made these videos so that parents can help students who “find the math lessons confusing.” The lessons are taught by a local public school math teacher:[799]

Addition Using Base 10 for 1st Grade & Older

Subtraction Using Place Value Chart (2nd Grade)

* CCSSI asserts that the Common Core standards are “research- and evidence-based.”[800]

* In October 2015, Just Facts asked CCSSI to provide “specific studies” that prove the math strategies above are effective.[801] CCSSI responded but did not provide such research.[802] [803] [804]

* The Common Core math standards compel students to explain “why a particular mathematical statement is true or where a mathematical rule comes from.”[805]

* The following sample question and answer are from a teaching guide for 3rd grade Common Core math from the North Carolina Department of Public Instruction:

* Per W. Stephen Wilson, Ph.D. mathematician, professor of mathematics at Johns Hopkins University, and Common Core supporter:[807] [808]

* Per CCSSI:

* In October 2015, Just Facts asked CCSSI to provide “specific studies” proving that forcing student to verbalize “why a particular mathematical statement is true” improves their math education.[811] CCSSI responded but did not provide such research.[812] [813] [814]

* The Common Core math standards require students to solve math problems by using “concrete models,” “drawings,” and “objects.”[815] The following video shows an example of this:

Homework Helper: Division with a Remainder (4th Grade & Up)

* Per a 1989 meta-study of student learning styles published in Educational Leadership and republished in 2002 in the California Journal of Science Education:

* CCSSI asserts that the Common Core standards are “for the benefit of all students.”[818]

* In October 2015, Just Facts asked CCSSI to provide “specific studies” that prove drawing pictures and using objects improve students’ math abilities.[819] CCSSI responded but did not provide such research.[820] [821] [822]

* The complete Common Core standards for “English Language Arts & Literacy in History/Social Studies, Science, and Technical Subjects” are available here.[823]

* Sandra Stotsky was the only expert on K–12 English language arts (ELA) standards who served on Common Core’s validation committee.[824] The validation committee report states that she is an:

* Stotsky refused to certify the standards and has been critical of them.[826] [827]

* Per CCSSI, the ELA standards:

* The ELA standards assert that “a particular standard was included in the document only when the best available evidence indicated that its mastery was essential for college and career readiness in a twenty-first-century, globally competitive society.”[835]

* CCSSI states that the Common Core standards are “not a curriculum.”[836]

* Per a 2003 academic book about middle school education standards:

* In 2009, Bill Gates, the primary financial backer of Common Core,[838] wrote that “identifying common standards is not enough. We’ll know we’ve succeeded when the curriculum and the tests are aligned to these standards.”[839]

* In 2010, the Common Core validation committee wrote that “alignment of curricula and assessments to the Common Core State Standards … will be essential to the staying power and lasting impact of the standards.”[840]

* In 2014, Bill Gates wrote:

* CCSSI asserts that the Common Core standards “do not dictate how teachers should teach.”[842]

* In 2014, Bill Gates wrote that the Common Core standards “are a blueprint of what students need to know, but they have nothing to say about how teachers teach that information.”[843]

* The Common Core ELA standards state that they “do not mandate such things as a particular writing process or the full range of metacognitive strategies that students may need to monitor and direct their thinking and learning.”[844] [845] The Common Core math standards do not contain a similar statement.[846]

* The Common Core math standards dictate the specific teaching processes and learning strategies shown in the examples above.

* Mathematician and Common Core supporter Hung-Hsi Wu has written that the Common Core math standards “say explicitly what needs to be taught” about the “process of reasoning” for solving equations.[847] In a commentary for American Educator, Wu detailed how Common Core requires the use of certain processes for adding fractions and mandates that these processes be taught over three years from grades 3 through 5. The first part of the 3rd grade teaching process is as follows:

* According to a math framework adopted by the Los Angeles County Office of Education and sponsored by Bill Gates:[849] [850]

* This framework asserts that, “White supremacy culture shows up in math classrooms when students are required to ‘show their work’ ” and instructs teachers to practice “how to answer mathematical problems without using words or numbers.”[852]

* For more facts about the impact of Common Core on teaching processes, see the forthcoming section on standardized tests.

* Tests (standardized and otherwise) can be used to:

* Per a 1980 academic book on the U.S. education system:

* When parents and governments don’t have access to valid information about student outcomes, school employees have leeway to minimize their workloads and favor their own interests over that of the students. Per a 2005 paper in the journal Education Economics, standardized exams can help remedy this problem “by supplying information about the performance of individual students relative to the national (or regional) student population.”[861] [862]

* Standardized tests can provide valid information about student outcomes if they accurately measure the desired effects of education. In education literature, this is called test validity. Per the Encyclopedia of Educational Psychology:

* Per the Encyclopedia of Measurement and Statistics:

* In 2010, the Obama administration awarded $330 million to two state-led consortiums to develop standardized tests that are aligned to Common Core:[865]

* In 2011, the Obama administration announced that it would exempt states from various requirements of federal education law if the states adhered to four conditions. The first of these was to adopt “college- and career-ready standards” and administer standardized tests aligned with these standards.[868] [869] [870] CCSSI refers to Common Core as “college- and career-readiness standards.”[871]

* Among the 46 states that adopted the Common Core standards, at least 26 became members of the PARCC consortium at some point, and at least 31 became members of the SBAC consortium at some point.[872] [873]

* In the 2014–15 school year, the first time the PARCC and SBAC tests were administered, 11 states and the District of Columbia used the PARCC exam, and 18 states used the SBAC exam.[874] [875] [876]

* Since the 2014–15 school year, several states that previously used the PARCC and SBAC exams have announced that they will not use them in the future.[877] [878] [879] [880] [881]

* SBAC maintains a list of states that are current members of the consortium.[882]

* PARCC used to maintain a list of states that were members of the consortium but no longer does so.[883] Per Education Week:

* Per a 2001 book on educational assessments published by the National Academies of Science:

* David Coleman was a lead writer for the Common Core ELA standards, a cofounder of an organization that “played a leading role in developing” the standards, and one of the key people who lobbied Bill Gates to fund Common Core.[887] [888] [889] In 2011, Coleman stated that the Common Core standards:

* In 2012, Coleman became president of the College Board, the organization that produces the SAT college entrance exam and Advanced Placement tests.[891] [892] [893] [894]

* In 2013, Coleman announced that the College Board was going to “redesign the SAT” to “prepare students for the rigors of college and career.”[895]

* In 2014, the College Board published a “conversation guide” for the redesigned SAT that posed the question, “Is the SAT aligned to the Common Core?” The guide answered:

* In March 2016, the redesigned SAT replaced the former version.[897]

* Homeschooling is the oldest form of education, and it was common practice until public schools became prevalent in the mid-1800s.[898] [899] [900] [901]

* In 2019, approximately 1.46 million children or 2.8% of K–12 students in the U.S. were homeschooled. These figures are not categorical, because some of these students also took some classes and played sports in public and private schools and colleges.[902] [903] [904]

* Depending upon their level of education, parents homeschooled their children at the following rates in 2019:

* Homeschooling is legal throughout the U.S. with widely varying state regulations on it. In the state of Washington, parents must be certified as teachers in order to homeschool.[906] [907] [908] [909]

* Homeschooling is permitted in most nations.[910] Germany has generally prohibited homeschooling since 1938 when the Nazi government enacted a law that effectively banned it.[911] [912] [913] Some other nations that ban or strictly limit homeschooling include Bulgaria, Greece, and the Netherlands.[914]

* A 2007 survey of parents who homeschool their children found that they did so for the following reasons:

|

Reason |

Portion of Parents |

|

Concern about the school environment, such as safety, drugs, or negative peer pressure |

88% |

|

Desire to provide religious or moral instruction to their children |

83% |

|

Dissatisfaction with academic instruction at other schools |

73% |

|

Desire to take a nontraditional approach to education |

65% |

|

Increased family time, financial considerations, flexibility to travel, or lack of proximity to an appropriate school |

32% |

|

Having a child with special needs “other than a physical or mental health problem that the parent feels the school cannot or will not meet” |

21% |

|

Having a child with a physical or mental health problem |

11% |

* In 2010, the journal Academic Leadership published a nationwide study of 11,739 homeschooled students during the 2007–08 school year. It found that parents spent a median of $400 to $599 per student on “textbooks, lesson materials, tutoring, enrichment services, testing, counseling, evaluation,” and other incidentals.[916] [917] Regarding these findings:

* The same study in Academic Leadership examined the academic performance of 22,584 homeschooled students who took standardized tests administered by three major testing services. This was the broadest sample of homeschooled student test scores ever studied. The researcher found that the average performance of these students ranked in the top 20% of all U.S. students in each of the five academic disciplines examined:

|

Subject |

Average National Ranking |

|

Reading |

87% |

|

Language |

81% |

|

Math |

80% |

|

Science |

82% |

|

Social Studies |

80% |

* Regarding the findings above, the paper documents that “the above-average nature of these achievement test scores is also consistent” with nine other similar studies. Per the study’s author, Brian D. Ray (Ph.D. in science education):[927]

* Per the Encyclopedia of Education Economics & Finance (2014):

* Digital learning involves the use of computerized technologies to increase the effectiveness of education or reduce its costs.[931] [932]

* Forms of digital learning include (but are not limited to):

* In the 2019–20 school year prior to the Covid-19 pandemic,[944] 17 states had publicly funded online K–12 schools that allowed students to take supplemental courses. Students took more than 1 million courses through these schools.[945] [946]

* With regard to fully online K–12 schools—primarily operated without physical buildings—that attract students from across districts:

* With regard to college students:

* In 2013, the journal Teachers College Record published an analysis of 45 experimental (and quasi-experimental) studies that measured 50 effects of online and blended learning versus traditional face-to-face classrooms. These studies included K–12 students, college students, and people receiving job-related training. The authors found that:

[1] Book: The SAGE Encyclopedia of Educational Technology. Edited by J. Michael Spector. Sage Publications, 2015. Article: “Adaptive Learning Software and Platforms.” By Dr. Kinshuk. Pages 7–10.

Page 9: “Various cognitive abilities of students are crucial for learning. Examples of these abilities include working memory capacity, inductive reasoning ability, information processing speed, associative learning skills, metacognitive skills, observation ability, analysis ability, and abstraction ability.”

[2] Paper: “The Importance of Noncognitive Skills: Lessons from the GED Testing Program.” By James J. Heckman and Yona Rubinstein. American Economic Review, May, 2001. Pages 145–149. <www.jstor.org>

Pages 145–146:

Studies by Samuel Bowles and Herbert Gintis (1976), Rick Edwards (1976), and Roger Klein and others (1991) demonstrate that job stability and dependability are traits most valued by employers as ascertained by supervisor ratings and questions of employers although they present no direct evidence on wages and educational attainment. Perseverance, dependability, and consistency are the most important predictors of grades in school (Bowles and Gintis, 1976).

[3] Encyclopedia of Education Economics and Finance. Edited by Dominic J. Brewer and Lawrence O. Picus. Sage Publications, 2014.

Page 498:

Omitted variable bias (OVB) occurs when an important independent variable is excluded from an estimation model, such as a linear regression, and its exclusion causes the estimated effects of the included independent variables to be biased. Bias will occur when the excluded variable is correlated with one or more of the included variables. An example of this occurs when investigating the returns to education. This typically involves regressing the log of wages on the number of years of completed schooling as well as on other demographic characteristics such as an individual’s race and gender. One important variable determining wages, however, is a person’s ability. In many such regressions, a measure of ability is not included in the regression (or the measure included only imperfectly controls for ability). Since ability is also likely to be correlated with the amount of schooling an individual receives, the estimated return to years of completed schooling will likely suffer from OVB.

[4] Report: “Improving Health and Social Cohesion through Education.” Organization for Economic Cooperation and Development, Center for Educational Research and Innovation, 2010. <www.oecd.org>

Pages 31–33:

(a) Reverse causality

One source of endogeneity stems from the possibility that there is reverse causality, whereby poor health or low CSE [civic and social engagement] reduces educational attainment. Poor health in youth might interfere with educational attainment by interfering with student learning because of increased absences and inability to concentrate. It may also lead to poor adult health, thus creating a correlation between education and adult health. Similarly, low CSE such as lack of trust and political interest might also reduce educational attainment. For example, a family with low CSE might reduce their involvement with schools, which might lead to poorer student outcomes.7

The bias due to reverse causality can be re-cast as an omitted variable problem after considering timing issues. Since health and CSE tend to persist over time, past health or CSE can be an important determinant of current health or CSE. Thus, past health or CSE is an omitted variable in equation (1) which is captured by the error term. The extent to which omitting past health or CSE will lead to an omitted variable bias depends on the extent to which past health or CSE is also correlated with the included variable Education. Because the current stock of education depends on past decisions about investments in education, reverse causality generates a correlation between past health or CSE and the individual’s current stock of education.8 If the estimated coefficient picks up the effect of past health or CSE … will be biased towards overestimating the causal effect of education.

(b) Hidden third variables

The second source of endogeneity comes from the possibility that there might be one or more hard-to-observe hidden third variables which are the true causes of both educational attainment and health and CSE.9 In the context of the education–earnings link, the most commonly mentioned hidden third variable is ability.10 The long-standing concern in this line of research has been that people with greater cognitive ability are more likely to invest in more education, but even without more education their higher cognitive ability would lead to higher earnings (Card, 2001). More recently, non-cognitive abilities such as the abilities to think ahead, to persist in tasks, or to adapt to their environments have been suggested as important determinants of both education and earnings outcomes (Heckman and Rubinstein, 2001).

In the context of the education–health link, Fuchs (1993) describes time preference and self-efficacy as his favorite candidates for hidden third variables. People with a low rate of time preference are more willing to forego current utility and invest more in both education and health capital that pays off in the future (Farrell and Fuchs, 1982, Fuchs, 1982). A classic example is the Stanford Marshmallow Experiment in which 4 year-olds were given the choice between eating the marshmallow now or waiting for the experimenter’s return and getting a second marshmallow. When these children were tested again at age 18, Shoda and others (1990) found a strong correlation between delayed gratification at age 4 and mathematical and English competence. Similarly, people with greater self-efficacy, i.e. those who believe in their ability to exercise control over outcomes, will be more likely to invest in schooling and health. Most studies of the schooling–health link use data sets that do not contain direct or proxy measures of time preference and self-efficacy. Consequently, these variables are typically omitted when estimating equation (1). The resulting omitted variable bias again implies that … will be biased towards overestimating the causal effect of education on health.